About MedSup

What is MedSup or Medigap?

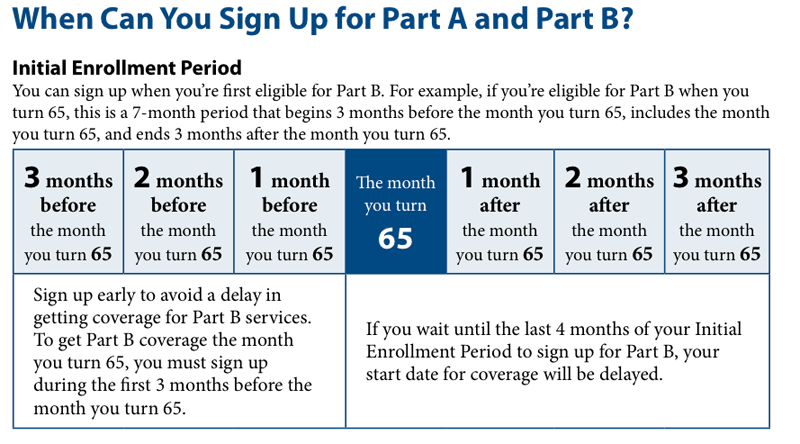

Part A (Hospital Insurance) covers most medically necessary hospital, skilled nursing facility, home health and hospice care. It is free if you have worked and paid Social Security taxes for at least 40 calendar quarters (10 years); you will pay a monthly premium if you have worked and paid taxes for less time. Part B (Medical Insurance) covers most medically necessary doctors’ services, preventive care, durable medical equipment, hospital outpatient services, laboratory tests, x-rays, mental health care, and some home health and ambulance services. You pay a monthly premium for this coverage. We offer Medicare Supplement (Medigap) plans that are designed to pay some or all of the eligible expenses not paid for by the original Medicare Part A (hospital coverage) and Medicare Part B (medical coverage). While Medicare has been of tremendous benefit to millions of older Americans since its inception in 1965, there are gaps in both Medicare Part A and Part B coverage that can impose a substantial financial burden. That’s why you should consider a Medicare Supplement plan. Medicare Supplement policies available include plans available in your state. The quote and brochure we send you will include which plans are available. These plans provide varying amounts of coverage, with Plan A offering basic benefits, and other plans offering more comprehensive coverage. Eligible Expenses are those costs that are deemed medically necessary by Medicare. Your Benefit Period (Medicare Part A) begins the day you go to a hospital or skilled nursing facility. The benefit period ends when you haven’t received any hospital or skilled nursing facility care for 60 days in a row. If you go into a hospital after one benefit period has ended, a new benefit period begins. We do not limit the number of benefit periods you can have. The Deductible is the amount you must pay for Medicare approved expenses before Medicare begins to pay. For Medicare Part A, your deductible applies to each benefit period. For Part B, the deductible applies at the beginning of each year. Most of the available plans pay your deductible for you. Coinsurance is a percentage of Medicare approved expenses not paid by Medicare. Open Enrollment is a one-time six-month period that begins the first day of the month in which you are both 65 or older‡ and are enrolled in Medicare Part B. During your Open Enrollment period: Planning begins with requesting a quote or apply today.

|

![]()

![]()